John Davidson's Economic Comments

Economic releases were largely positive this week, but the capital markets reacted negatively to the post-Fedearl Open Market Committee meeting comments by Federal Reserve Chairman Ben Bernanke. The capital markets have started to price in the long-anticipated tapering or ending of the quantitative easing (bond purchases) by the Federal Reserve. There were few safe harbors. The Japanese market was an exception in posting a positive return when elsewhere equity markets declined. Government and credit bond markets also fell. Oil and metals commodity prices declined on the week. In contrast, the U.S. dollar strengthened.

Perspective:

My quote from last week's Comments, "A portfolio in cash is safe, but that's not what investment portfolios are built for." was not well-timed given this week's decline in the stock and bond markets. U.S. dollar cash was one of the few safe havens. To clarify, my sailing analogy allowed for the reefing of the sails to reduce exposure. Adding cash to a fixed income portfolio reduces the interest rate (duration) exposure (as well as the yield). Adding cash to an equity portfolio reduces the exposure to the equity market (beta). Adding cash is different from going all-in to cash. Making a marginal change in allocation to cash allows for less than perfect timing. In my 35+ years as an institutional investor I have heard market timers claim to have gotten out of the market in advance of a decline and have heard market timers claim to have invested in advance of a bull market, but I have not seen evidence of success in getting in and out of the markets.

At lunch this week another former fixed income portfolio manager posed the question, "Does it matter whether or not the Fed tapers or just stops buying bonds cold turkey?" This week's capital market reaction would support the argument that it does not matter. By the time the Fed takes its action, market prices will have already adjusted to the new policy.

Economic Releases:

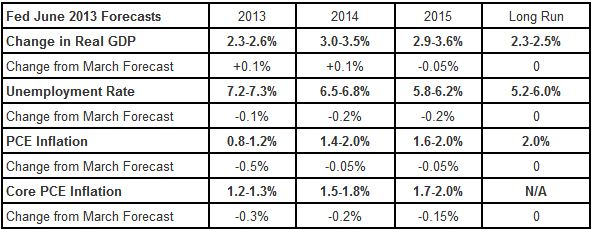

At the conclusion of this week's FOMC meeting the Federal Reserve made no changes in rates, bond purchases or policy thresholds (6.5% unemployment, 2.5% inflation). The June forecasts (shown in the table below) should have been positive for the U.S. economy, but the capital markets focused on the chairman's implicit shorter timetable for the tapering of quantitative easing. Chairman Bernanke did not intend to announce a change in policy, but the capital markets reacted as though he did.

The Federal Reserve released its June forecast for the U.S. economy as shown in the table below. As compared to the March forecast, GDP growth is a tick stronger, the unemployment rate is lower, and inflationary pressures are expected to be less than they were projected in the March forecasts.

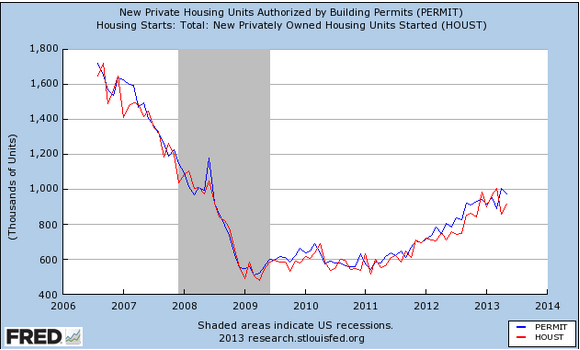

One recent source of strength in the U.S. economy has been housing. U.S. Housing Starts (red in the chart) increased to 914,000 while Permits (blue in the chart) eased to 974,000 in May. The chart shows that the trend in Starts and Permits has been positive over the past few years, but still pales in comparison to the pre-Great Recession era. In other housing news, Existing Home Sales rose to 5.18 million in May, a 4.2% increase from April and a 12.9% increase from a year ago. The National Association of Home Builders Housing Market Index rose 8 points to 52, crossing the threshold, 50, from pessimistic to optimistic, in June.

Other Economic Releases

This week's Initial Jobless Claims in the U.S. rose above expectations to 354,000; the four-week average rose to 348,250. The Markit Flash PMI Manufacturing Index rose to 52.2 in June; the Philadelphia Fed Survey leaped 17 points to 12.5 and the Empire State increased 9 points to 7.84 in June. The CPI report showed that inflation has remained well contained; May's CPI increased just a tick; even without the more volatile food and energy components, the Core CPI rose only +0.2%.

The European Union Markit Flash report for June increased a point to 48.9, but remained in the contraction zone (below 50); Germany's flash report gained a point to 50.9 with Services at 48.7 and Manufacturing at 48.7; France's flash report rose to 46.8, but remained in the contraction zone. China's Flash PMI slipped a point to 48.3.

Germany's Zew Survey for Current Conditions slipped to 8.6 while Business Expectations rose to 38.5; both were less than consensus. UK's Retail Sales rose 2.1% in May, well above consensus and a strong rebound from the -1.1% decline in April. UK inflationary pressures remained well contained in May; CPI rose +0.2%; PPI for output was flat while PPI for Input fell -0.3%.

Equities Markets:

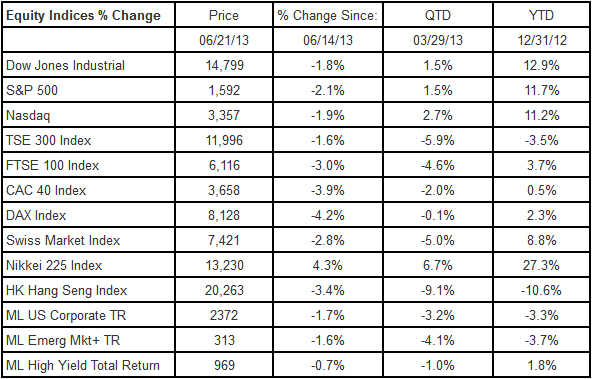

Equity markets fell across the globe; only the Japanese Nikkei posted a positive return for the week. Widening credit spreads and rising bond yields led to negative returns in the ML bond markets as well (note that they are reported on a one-day lag, i.e. Thursday-Thursday).

Bond Markets:

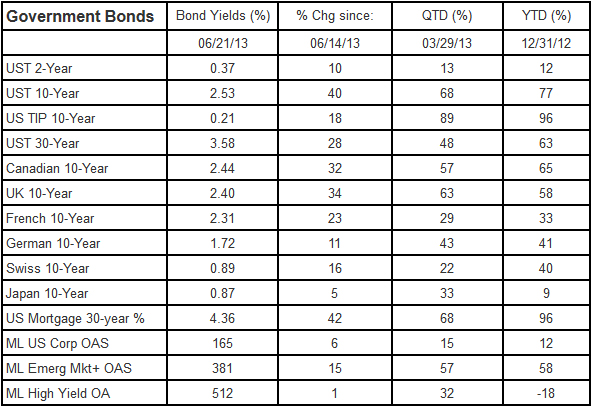

Government bond yields rose and credit spreads widened in anticipation of the end of Central Bank bond purchases. Previously, bonds have been a good diversifying asset against declines in equity prices, but not this week.

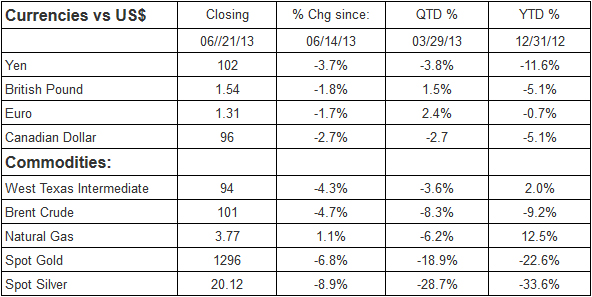

Currencies & Commodities:

The U.S. dollar rose against the other currencies this week. For the U.S. investor in the Japanese equity market, the decline of the Yen would have offset most of the gain in the Nikkei. Those that hawk gold as a safe haven may have been chagrined to see that gold fell more than stocks this week; in fact the YTD -22.6% decline does not stand up too well to the double digit increase in U.S. equity markets.

-----------------------------------------------------------------

Who is John Davidson?

John W. Davidson, CFA, started writing these Comments over a decade ago as a personal discipline when he was promoted to chief investment officer from portfolio manager.

Most recently, he was the president of PartnerRe Asset Management Corporation, responsible for the management of PartnerRe's invested assets, which grew from $4 billion to $12 billion during his tenure. After joining PartnerRe in the fall of 2001, he hired the staff, built the trading floor and created the infrastructure to manage both fixed income and equity assets internally. He retired from PartnerRe at the end of 2008 and moved to Maine.

He has more than 35 years of industry experience, including positions with investment management responsibility for separate institutional accounts, mutual funds, trusts, and insurance assets. Prior to joining PartnerRe, he served as president and chief executive officer of two other investment management companies. For various companies he has held positions as chief investment officer, chief economist, head of fixed income, and portfolio manager. As a portfolio manager, Davidson managed and traded U.S. Government Securities as well as futures and options on fixed income instruments.

His real world experience is backed by a strong academic foundation, which includes earning a Master of Business Administration in finance and a Master of Arts in mathematics from Boston College, as well as a Bachelor of Arts, cum laude, in economics from Amherst College. He holds the professional designation of chartered financial analyst.

His experiences and credentials have brought him to the public as a television commentator and conference speaker. In addition to his frequent past appearances on CNBC, CNNfn, Bloomberg TV and Yahoo FinanceVision, he has appeared as a special guest on Wall $treet Week with Louis Rukeyser. Reuters, Bloomberg and other business press services often quote his views on the market. He has taught CFA preparation programs, as well as other courses offered by the Stamford and Boston CFA Societies, and courses at the National Graduate Trust Officers' School.

Davidson is a natural leader in both his professional and personal life, having developed those skills early in his career as a Naval Officer. He spent three years on active duty, which included a year on the rivers of Vietnam, and 24 years in the Naval Reserves, from which he retired as a captain in 1994.

Davidson is treasurer and board member of the Camden Conference. He is treasurer of the Maine Conference of the United Church of Christ, serving on the executive committee and the coordinating council, the governing board of the conference. He is also on the investment committee of the Pen Bay Health Foundation.

In his leisure time, he is an active sailor, tennis player and skier. With his wife, Barbara, he renovated a 100+-year-old home in Camden, where they enjoy spending time with their two golden retrievers and having visits from their five children. He can be reached at jwdbond@me.com.