Maine enters recession in wake of virus. This is what five experts think about Maine’s economic recovery.

")

The recession arrived not as a slow and predictable financial decline, but as a cliff.

Economists agree that Maine is experiencing an “unprecedented” economic downturn due to the coronavirus pandemic that has forced businesses to close and massive, rapid layoffs of employees. There is no past economic event that they can look to for guidance that matches the current decline in its scope or speed.

But with mixed messages from state and federal authorities on whether it is time to reopen businesses, Pine Tree Watch spoke with four economists and one finance professor with intimate knowledge of Maine to understand where the state’s economy is headed and what past recessions may — or may not — tell us about how it will recover.

Interviewed individually, their responses revealed three common threads:

• A large, rapid downturn in Maine’s economy followed the arrival of a novel coronavirus that causes the respiratory illness COVID-19. While there is no single definition of “recession,” it is likely that Maine has already fallen into one.

• Unemployment is a wild card in this economic downturn. Unemployment typically lags behind a financial decline, but it is a leading indicator this time. Whether unemployment is temporary or permanent will play an important role in how long it takes Maine’s economy to rebound.

• Reopening will be dictated by consumer confidence in the state’s ability to control the spread of the virus through testing and contact tracing. Confidence may be restored slower for places such as restaurants or sports venues than large stores, where it is easier to be physically distant from others.

The current decline in Maine’s economy is first and foremost a public health crisis, said State Economist Amanda Rector.

“Until we manage to get the public health crisis under control we really don’t have a way to understand how deep the economic crisis will be or how to really bring the economy right back on board,” said Rector, who has been in her post since 2011.

The focus of the past several weeks has been on how to keep Maine residents and businesses afloat during the economic shutdown until the public health crisis was under control. With the number of active coronavirus cases still climbing but a surge of hospitalizations avoided at the moment, Rector and one additional analyst have begun piecing together a new picture of Maine’s economy.

To start: a bit of good news. The underlying conditions of Maine’s economy were in “reasonably good shape” in late 2019 and early 2020. Maine has money in the budget stabilization fund to get it through this fiscal year, which ends on June 30, Rector said.

There will be a hole in next fiscal year’s budget, but how large that will be is yet to be determined.

Maine received $1.25 billion in federal stimulus money from the Coronavirus Aid, Relief and Economic Security (CARES) Act to help cover some of the costs of fighting the coronavirus. This does not include additional money that went to hospitals, universities and federally qualified health centers.

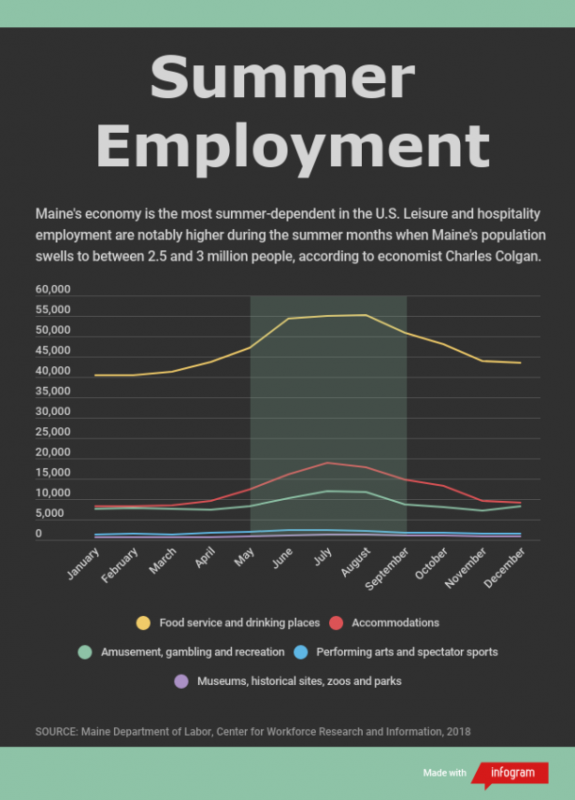

With Memorial Day weekend just a week away, now is when Maine would typically see its population swell to 2.5 to 3 million people as visitors flock to beaches, lobster shacks, campgrounds and Acadia National Park.

Maine has the most summer-dependent economy in the U.S., with leisure and hospitality employment notably higher in the summer, said Charles Colgan, professor emeritus at the University of Southern Maine and research director for Center for the Blue Economy.

While leisure and hospitality make up a significant portion of Maine’s employment — almost 11 percent, according to the latest Maine Economic Growth Council report — not all of Maine’s economy is dependent on tourism, said Steven Cunningham, professor of management and economics at Husson University. A year without summer tourism will have an effect, but it is not the only pillar holding up Maine’s economy.

Economists are staring down the barrel of two different nightmare scenarios, simultaneously. The first is a prolonged shutdown of the economy, in which businesses do not recover and unemployment becomes permanent. The other scenario has Maine businesses opening too quickly and a sudden resurgence of infections that require another shutdown.

Gov. Janet Mills convened an Economic Recovery Committee on May 6 to bridge the state’s reopening plan to its 10-year economic plan.

The recovery committee will focus on identifying barriers that could stand in the way of rapidly kickstarting economic growth and stimuluses that could aid it as the state economy restarts, said Laurie Lachance, president of Thomas College and a former state economist. She will co-chair the recovery committee with Tilson CEO Josh Broder.

Maine businesses will not be able to operate as they always have, and this needs to be a period of innovation, she said.

“Prosperity is not about your form of government, your economic underpinnings, your access to natural resources — it’s not about that. It’s about your people’s ability to innovate and draw on those things that are authentically yours,” Lachance said.

“The way we come out of it is taking that rich knowledge and body of experience and recreating the future by innovating it to the new products and services. That’s where we find our greatest success.”

Unemployed amid uncertainty

Between the discovery of the first case of COVID-19 on March 12 and the first death on March 27, employers shut their doors and laid off or furloughed tens of thousands of employees.

The resulting spike in unemployment broke economic forecasting models. The Maine Department of Labor reported a 3,285% increase in initial claims of unemployment between the week ending March 21 and the week before. The next six weeks continued to shatter records.

It doesn’t take bar charts and trend lines to see what the coronavirus has done to employment in Maine.

J. Douglas Wellington, a finance professor at Husson University in Bangor, hasn’t traveled far beyond his Castine home since Mills put the stay-at-home order in place. But a friend’s description of Ellsworth as a ghost town, with stores dark and parking lots empty, stuck with him.

“The number of new jobless claims — that’s very concerning,” Wellington said.

At Husson, Wellington created a stock index of 29 publicly traded companies that are headquartered in Maine or have a significant number of employees in Maine that he uses to analyze the state’s economic well-being. An Associated Press report on unemployment claims caught his attention last week. While the number of claims decreased in most states, they rose in six states including Maine, where the increase was 111.1 percent.

“We had the dubious distinction of having the largest increase in weekly jobless claims, when 44 states were already reporting decreases in jobless claims,” Wellington said. “I’d certainly like to see that number go down.

“As the jobless claims go down, as the unemployment rate goes down, obviously, that’s indicating we’re coming back,” he added.

Just as the downturn was visible in the empty streets of Ellsworth, evidence of recovery will be tangible in everyday life, too, Wellington said. His wife reported that stores and parking lots in Bangor were “as full as they could be with social distancing,” when she traveled there last week.

“Some of those not-really-economic indicators are also going to give a feel for whether or not we’re coming back,” Wellington said.

One of the biggest unknowns is when those who are unemployed will be able to return to their jobs. If furloughs are temporary and workers can return to their pre-pandemic jobs, then the economy can pick up quicker, Rector said. If unemployment is permanent, then the recovery will be delayed due to time lost to hiring and training new employees.

Multiple economists interviewed by Pine Tree Watch shared a common concern about the future of small businesses in Maine. The small businesses that make New England towns “interesting” and “quaint” offer a lot of employment but they are also one of the largest vulnerabilities in the state’s economy, Cunningham said.

“The problem is that many of these businesses do not have large cash reserves, they are living on their cash flow,” Cunningham said. “When you have an interruption to the income stream, it’s devastating, which means that the longer that the shutdowns of the economy go on, the worse it’s going to be because they simply don’t have the reserves to make it for a long period of time.”

Either the stores will never reopen or a portion of their customer base will not return, he predicted.

Where unemployment hurts is in the home. Lachance describes her upbringing as one with “humble roots” with her first year at Bowdoin College costing as much as her parent’s house. In her nearly four decades as an economist, she has not seen worse unemployment.

Whether economists officially label the current downturn a recession or not, it’s going to hurt. People are going to feel like they’re in a recession, she said.

Frustration has already boiled over with approximately 100 people protesting outside the capitol demanding Maine reopen. Republican state lawmakers too have called for the legislature to reconvene to consider the removal of emergency powers from Mills.

Mills extended the civil state of emergency in Maine for an additional 30 days to June 11 on Wednesday.

The federal government is currently propping up the U.S. economy with zero percent interest rates and federal borrowing. How long Maine can afford to stay closed depends on what Congress decides to do next, Colgan said.

The Federal Reserve is “pouring money” into the economy at almost “unprecedented” levels, which has increased the U.S. money supply by slightly less than 20 percent in roughly the past month, Cunningham said. That’s equal to a year’s increase to the money supply.

Cunningham was on the Federal Reserve’s Board of Governors in the late 1980s, where he worked with price data to predict inflation rates and optimize monetary policy. USA Today broke down how money goes from newly created electronic dollars to securities to actual money in a bank on Tuesday.

Cunningham cautioned that it’s easy to cling to unemployment data as the key metric to gauge how the economy is doing because it comes out every week. But bigger-picture data, like the GDP, which is released quarterly, can be more insightful — it just takes longer to report.

Today’s unemployment conditions were caused by the government sending everyone home from work.

“We made this data happen. We said go home. Don’t go to work,” Cunningham said.

What frustrates Colgan, whose research centers on coastal economies and flooding, is that what is happening in Maine and the U.S. more broadly is exactly what economists predicted would happen during a pandemic.

“The whole thing was not only foreseeable, it was foreseen,” Colgan said. “We know that one of the major effects of climate change will be to radically alter disease vectors and make these kinds of events more common. This is a once-in-a-century event. This could easily become once in every 20 years.”

It was right to treat the virus as a hazard but not its consequences, he said. The economic fallout of a pandemic is all man made.

‘Everything’s open, olly olly oxen free’

The shutdown of Maine’s economy has caused unemployment, but it’s also slowed the spread of the virus.

“The whole strategy with COVID-19 is to keep people from moving around and transmitting it,” Colgan said.

According to Colgan, to get a robust economy running again will depend on Maine’s medical and public health systems and how quickly the state can begin testing and contact tracing, which are the “bread and butter of epidemic containment.”

Because if the state rushes to reopen at the expense of public health, and has to close again, that is going to be more detrimental to the economy, Rector said.

Mills announced a strategic partnership with Westbrook-based IDEXX Laboratories, Inc. on May 7 to increase Maine’s weekly testing capacity by approximately 5,000 tests a week. The following day she released a revised rural reopening plan to open businesses in counties where there was no evidence of community transmission of the virus.

Retail stores reopened on Monday to limited customers and with enhanced cleaning and touch-free transactions in all but Androscoggin, Cumberland, York and Penobscot counties. Restaurants are scheduled to open to dine-in services on May 18, as are campsites and certain outdoor recreation businesses to Maine residents or out-of-state visitors who have completed a 14-day quarantine.

More testing supplies is good, but still not enough.

“That will help. Now triple it and triple it again, and you might begin to make a dent in the effects on tourism,” Colgan said. “It’s numbers. It’s just sheer numbers. We really can’t pull over everybody as they come through the York tolls … and have them take a test. It might be a good idea, but we can’t do it.”

Even if Mills were to lift her executive order and reopen all Maine businesses next week, customers would still need to feel comfortable shopping or dining.

“Let’s say the state says, ‘Everything’s open, olly olly oxen free.’ Are you going to go sit in the restaurant? Ehh, I don’t know. At a minimum, there’s going to be fewer people going into the restaurants for a while,” Cunningham said.

It’s called consumer confidence, and it’s tricky because it hinges on whether people feel safe.

At Thomas College, the customers are 18-to-24-year-old students and their parents. Lachance made the difficult decision to move students online for the remainder of the spring semester after reading a “heartfelt, painful” email from one set of parents, who begged her to close the college and send their daughter home. It kept her up that night.

“Fear makes it hard. And when it’s your child, it becomes very personal very fast,” Lachance said.

Thomas College plans to reopen for the fall semester for in-person instruction, but with fewer students per classroom and extra dorms set aside to quarantine students who may be sick or exposed to the virus. There will also be additional cleaning and counseling staff added to protect student health.

One of the longest-running surveys of registered voters in Maine showed that more than one-third (38 percent) believed the country was “striking the right balance” between minimizing the health impact of the coronavirus and the need for a healthy economy in March. Another third said the country was “too worried about the economy.”

The survey also found that 9 of 10 Mainers had avoided public places as a result of the coronavirus, such as restaurants.

“You see substantial evidence from the survey research that people don’t care what’s open, they’re not going anywhere. That may be actually the biggest hurdle to all of this coming back together again. It’s not what the rules are, but what people feel is safe,” Colgan said.

During a normal recession, not a pandemic, economists could model and say, “Where this line crosses, we’ve got to be open,” Lachance said. But in the case of a pandemic, the ability of any business in any sector to operate depends on the health of employees and customers, she said.

How well social distancing can be implemented at stores, restaurants or sports venues will be crucial to building confidence; as will keeping the spread of the virus under control.

Businesses cannot open and be the purveyor of disease, because that will kill a business too, Lachance said.

“We can’t afford to stay closed long, but we can’t afford not to stay closed long enough to make the situation as safe as we can,” Lachance said. “There will be parts of this that we cannot prevent and we understand that. But to the extent that we can prevent the rapid transmission, we have to stay closed long enough to do that or we’ll do it at our own peril.”

Pine Tree Watch spoke with four Maine economists and one finance professor about vulnerabilities in the state economy and how it will get back on track. Below are each of those interviews.

Amanda Rector

Amanda Rector is the current Maine state economist. Starting in her role in 2011, she has advised former Gov. Paul LePage (R) and Gov. Janet Mills (D). Rector earned a master’s in Public Policy and Management from the Muskie School of Public Service at the University of Southern Maine. This transcript has been edited for length and clarity.

Samantha Hogan: I wanted to get your take on what you think are the vulnerabilities of Maine’s economy. And is the CARES Act the right tool to get Maine’s economy back on track?

Amanda Rector: One of the good things is Maine’s economy was actually in reasonably good shape going into this. A lot of the data we had from the end of 2019 indicated that Maine’s economy was pretty strong right up until the effects of this (pandemic) started to be felt. That means that a lot of the underlying conditions of the economy were in reasonably good shape.

We have money in the budget stabilization fund to help fill some of the potential budget holes that could appear. We don’t know exactly how much that’s going to be yet, but we imagine that there probably will be one. And, it will probably be more in the next fiscal year — the fiscal year starting in July.

A lot of the revenues that have been coming in even through March and April were still really pretty good, because they reflected conditions prior to (the pandemic). So, we’ve made it through most of the fiscal year in good shape from a budgetary and revenue standpoint.

The fact that Maine’s economy was in a pretty good state before this hit, if we can manage to keep people reasonably whole through this time of economic timeout, then when we’re ready to open things up again, hopefully, people are more able to step back into the roles and jobs they were in. Rather, if we were in a long period of decline before this picked up, then things would be much more challenging on the other side.

We just don’t know what this downturn and recovery are going to (be) until we have a sense of what the final trajectory of the public health crisis looks like.

Hogan: What economic signals would concern you right now? Are you watching for anything in particular?

Rector: One of the things that’s going to be really interesting in the coming weeks is to see on the unemployment front how many of these layoffs or furloughs are temporary.

In some cases, it could be that new claims are coming in but people have already gone back to work maybe because their employer took some of the Payroll Protection (Program) funding. So they have been called back already — even if they’re not physically there — they might be on payroll, at least.

How many are temporary versus permanent layoffs?

The more that things are just temporary — more of a furlough, people having to step away for a brief period and then coming right back — means that the economy will be able to pick up speed much more quickly. If it’s more permanent layoffs, that means it’s going to take a bit longer for businesses to gear back up again, because then they have to go through the process of rehiring, retraining and integrating the new person back into their workforce as opposed to bringing someone back in who already knows what they’re doing and can just hit the ground running.

Hogan: How long can Maine afford to stay closed?

Rector: This was driven by this public health crisis, and we need to make sure that we don’t fall into the trap of trying to open things up too quickly and lose all our hard-won gains on the public health front.

We want to make sure that we can get the economy going again in a manner that is not detrimental to the public health side, because if that happens and we end up having to take another step back again that is going to be more damaging to the economy.

I think really what we want to do is make sure that we can keep people and businesses as functional as possible in the short term while we deal with public health and then roll things out gradually. (While) making sure that we are doing everything the governor is talking about in terms of tracking and monitoring (and) making sure we’re not setting ourselves up for failure on the health side.

The federal government has come out with a lot of programs both on the monetary policy and the fiscal policy side around trying to make sure that we can tide people with business over through the public health crisis.

Hogan: Are we in a recession?

Rector: I don’t know. There are different definitions for a recession and certainly depending on how you’re defining a recession maybe we are, maybe we aren’t. I think clearly we’re in just an unprecedented economic situation.

How we end up defining that as we come through it — we may define it differently. We may change our definitions and terminology, because this is such an unusual event.

Often what happens is that things are slowing down, there’s less demand for goods and construction turns down. A lot of what’s happening now, instead, is that people cannot go out to restaurants and lodging has been decimated. It’s a very different industry (that was) hit.

Hogan: Coming out of the last recession, which companies, industries or sectors were crucial to Maine’s recovery? How will they play a role now?

Rector: You can’t really compare this with the Great Recession because it is such a different type of economic slowdown or contraction. All of the things that triggered the Great Recession are not what are happening now. So, the impacts were very, very different.

Professional and business services was one of the industries that continued to grow pretty much right straight through and has seen tremendous growth. That industry covers everything from law firms, architecture firms, waste management and temp agencies. It’s very broad in what gets collected in that industry sector, but that is one that has been growing pretty strongly.

I would imagine that given that a lot of those are easily translatable to remote work that that industry might continue to hold up well through this period.

Steven Cunningham

Steven Cunningham is a professor of management and economics at Husson University in Bangor. He has worked as an economist for more than 30 years, including as part of the Federal Reserve’s Board of Governors, where he helped optimize monetary policy in the late 1980s. Cunningham, who has lived in Maine for four years, is also a four-year board member of the Eastern Maine Economic Development Corporation. This transcript has been edited for length and clarity.

Meg Robbins: What are the vulnerabilities of Maine’s economy, and do you think the stimulus money from the federal CARES Act can stave off a recession?

Steven Cunningham: Before we discuss the vulnerabilities of Maine’s economy, I think it’s important to discuss the flip side of that question, the strengths of Maine’s economy.

A lot of people take the attitude that there’s a major reliance on leisure and hospitality. I think that’s a conventional wisdom that we are really tied to, and I don’t think that’s true. The data shows that the direct impact on the economy of those industries are around 10-12 percent. So while it is significant, it’s not as though the entire Maine economy is built on tourism. I don’t think that is as big an issue as one might think.

I think one of the risks is that we have a lot of small businesses in Maine, which are important to any economy. We find that small businesses and new businesses tend to produce a lot of employment and therefore that makes them important. The problem is that many of these businesses do not have large cash reserves. They are living on their cash flow, they are often relatively leveraged and when you have an interruption to the income stream, it’s devastating. Which means that the longer the shutdown of the economy goes on, the worse it’s going to be because they simply don’t have the reserves to make it for a long period of time.

This is exacerbated by the fact that in Maine — and we’re talking about before the pandemic and the shutdown occurred — 60 percent of households had less than $1,000 in the bank and roughly 70 percent had less than $5,000 in the bank, which is to say that many households in Maine, the majority of households perhaps, are one paycheck away from being homeless. They don’t have the reserves.

Again, this is a problem. We need to be saving more, but we haven’t. It’s become the American way.

If we look at the stimulus money, I don’t believe it’s going to be enough to avoid a recession. I mean, we just heard that the unemployment rate has gone to 14.7 percent nationally, and the U.S. lost over 20 million jobs in April. With numbers like that we have to believe that the second quarter is going to come in as a recession. The earliest data that we get on that won’t come in until a couple of months from now at the earliest, but I think it’s almost a sure thing that the second quarter, and probably third quarter, will be a recession. I think that boat has sailed.

But we have some help from these programs that are designed to help support households and replace incomes, and the Federal Reserve has increased the money supply by slightly less than 20 percent in the last month or so. That’s a year’s worth of money supply. They’re pouring money into the economy at almost unprecedented levels. So I think that this is going to be very, very helpful.

Robbins: What metrics are you turning to to get a sense of how the economy is doing? What would concern you and what would you find encouraging?

Cunningham: I think that we look at the unemployment data and job claims because we get this data fairly frequently. We don’t get GDP data very frequently, so it’s important to look at the data we actually have. And we’re seeing that there has been a lot of unemployment claims, 33 million in the last seven weeks or so, which is kind of a leading indicator.

We’re also seeing that the unemployment claims have dropped for five weeks in a row and in fact, it appears like they may have hit a bottom, so this makes sense. We told everybody to stay home. We closed the businesses, the people went over and they applied for unemployment. And now that’s done, mostly. Now they’re sitting and waiting to come back to work. It’s not a case where the economy is collapsing and people are continuing to flood out of the economy. We told a certain group of people in that economy to go stay home for a while, and they did, and they made the claims which they were supposed to. And so the assumption is they’ll come back when they’re told to.

Maine people in particular have a real Yankee work ethic. They come in, they work hard, they produce a lot. They’re highly skilled, highly educated. You couldn’t ask for better. You don’t have to ask them to come to work — they want to. Our unemployment rate before this pandemic was below the national average. One would expect that when they’re allowed to come back, they will, and they’ll come back strongly.

The demand is already there, consumer spending is already up, and if the stock market’s holding up, people’s sense of their wealth will be good. They won’t think that they’ve lost everything.

Robbins: How long do you think Maine’s economy can afford to stay closed?

Cunningham: That fits right into this. People are adjusting. People are enormously resilient and adaptable. A lot of changes that are going on in the economy were going on slowly, as they should. People were slowly adjusting to new technologies, to new ways of doing things, and they were in no hurry.

Now, we suddenly shut down big sections of the economy for three months, and as we continue with this shutdown, we are causing restructuring. Now people are having to find new ways to do things. Now they’re going online. Now they’re doing their schooling online. Now they’re buying from Amazon instead of the local shop they used to go to; they’re making adjustments.

But the longer the shop down the street stays closed, the more likely it’ll stay closed forever, because it has accumulated too much debt and it lost its position in the market economy. And if the shop winds up closing, that creates unemployment. So you have these structural shifts that occur the longer that the state stays closed, which now are going to have to be absorbed by the economy. That could make the recession go longer.

Now there’s going to be other issues with things like restaurants and services. Services have been the hardest-hit; we understand why that would happen because what services are you going to take advantage of during the shutdown when you have to have face-to-face contact with services? But restaurants — let’s say the state says, “Everything’s open, olly olly oxen free.” Are you going to go sit in the restaurant? Ehh, I don’t know. At a minimum, there’s going to be fewer people going into the restaurants for a while. So again, it’s going to be slower coming back.

The quicker we can walk away from the pandemic and get back to work, the quicker a recession will go away. But we also have to be worried about if we come back and then have a resurgence of the virus in the fall. If it were anywhere near like what we’re experiencing now, the economy’s already going to be weakened, all these structural shifts have already started to occur and it’s going to be more problematic. There’s no immediate indication that’s going to happen, but I’m just saying. That is a concern.

I don’t think the future is bleak, but I think that how long the recession will last and how severe it is will depend a lot on us.

Robbins: Looking back to the previous recession, which businesses, industries or sectors were crucial to Maine’s recovery, and how will they play a role now?

Cunningham: Well, I think that there’s a difference when you have a recession that is the result of a decline in demand and external supply shocks — that’s a very different thing than what we’re looking at right now. I think that Maine’s traditional industries are solid. I think that certainly our tourism, leisure and hospitality will be important. But I think the newer industries and technology industries are going to be important.

I think there’s a lot of pent-up demand. We have a lot of high tech that we can draw on that I think is going to be very important. I think as soon as people can leave Massachusetts and New York, they’re going to want to come north and spend some time in Maine and enjoy our beautiful climate and the good people and the shops and the New England scenery, and I think it will come back pretty quickly. I really think there’s a lot here. But we’ve got to get to a point where we can do that and you have to build confidence that we can do it safely, but we’ll get there.

Charles Colgan

Charles Colgan is a professor emeritus at the University of Southern Maine and research associate at the Center for Business and Economic Research. Colgan splits his time between South Portland, Maine, and Monterey, California, as the director of research for the Center for the Blue Economy at the Middlebury Institute of International Studies. Colgan served as the Maine State Economist from 1987 to 1989 and hosted an annual forecast of Maine’s economy between 1992 and 2015. This transcript has been edited for length and clarity.

Samantha Hogan: What makes Maine’s economy vulnerable? And, the money we’re seeing come into the state through the CARES Act, is that the right tool for Maine’s economy?

Charles Colgan: Maine used to be wildly different than the U.S. Fifty years ago, Maine’s economy was remarkably different than the U.S. It was way over-dependent upon manufacturing jobs, particularly low-wage manufacturing in clothing, shoes and textiles.

Over those 50 years, the most important change to the Maine economy, one which everyone remarks upon and kind of bemoans, is that the Maine economy is essentially a mirror image of the U.S. economy in terms of the types of jobs we have here today. We (Maine) have a relatively robust fishing and agriculture, but so does New York state and so does California. If you think of California as Silicon Valley and the movie industry, you haven’t been to the Central Valley or Salinas Valley near where I live and seen what agriculture is there.

We are very similar to the rest of the U.S. That’s a good thing and a bad thing.

The good thing is that we’ve moved into service jobs and professional and technical jobs of the kind that are much more likely to be kept alive during this recession because of technology. If this (coronavirus) had hit the 1970 Maine economy and we had to shut down factories, there would have been nothing left to replace it.

That means what will work for the whole U.S. will probably work for Maine.

Hogan: What economic signals would concern you right now? What are you watching for?

Colgan: In tourism and recreation, we are the most summer-dependent coastal state. The ratio between our summer tourism and recreation and our annual tourism and recreation employment is the greatest of all the states — about 34 percent higher in the summer than it is on average.

The beaches open, the hotels open and restaurants — the lobster shacks — open up. So, we have an entire portion of the tourism and recreation economy that only comes into existence in the summer. To me, this is the one big thing about Maine. Because (summer) is such a large portion of our tourism and recreation activities, that’s the one area I’m concerned about.

We don’t have a good estimate of the summer population in Maine, but it’s probably on the order of 2.5 to 3 million people, who come through Maine for some period of time. Our population doesn’t triple, because they’re not all here at the same time, thankfully.

But if the two-week quarantine orders were to stay in effect through September — which it very well might — then you can’t take that many people out of the consumer economy and not have a massive effect.

Hogan: How long do you think from an economic standpoint Maine can afford to stay closed?

Colgan: That all depends on how long the federal government is willing to let us stay closed.

Right now the economy is basically being supported by zero interest rates and massive federal borrowing. That’s what’s filling the hole. It’s not filling it very well, but it’s what’s filling the hole. How long and for how much the Congress is willing to keep filling the hole — instead of spending money to actually fix the hole — is outside what an economist can say.

Hogan: Is fixing the hole a vaccine?

Colgan: Fixing the hole is putting a patch in, which is testing and tracing. Fixing the hole means tearing down the wall and building a new one, which is the vaccine.

Hogan: Coming out of the last recession, which companies, industries or sectors were crucial to Maine’s recovery? How will they play the same role this time?

Colgan: Healthcare, government and education stayed relatively stable, and those were the foundations upon which jobs began to add.

The leading sectors coming back tend to be those dealing with durable goods, because they were the ones that tanked first. Essentially, you can put off buying a car, but eventually you’re going to buy a car. Once the economy began to get to the point that people started to have some confidence in it, they began buying cars again and car dealers started ordering cars and hiring salespeople and so on.

Tourism came back. Although the tourism effects were longer lasting than I think they probably should have been, largely because the recovery was stomped on by the austerity policies in Washington (D.C.).

One of the things that was surprising in the recovery from the Great Recession — that had not been true from the previous three or four recessions I’d been through — was that retail did not come back. It took a long, long time. And actually, retail employment as a whole has never returned to mid-2000s levels.

This is part of a long-term trend in the gradual reduction in retail employment in the retail sector. There’s a whole bunch of reasons for it. Much of it has to do with consumer preferences. Some of it’s Amazon and its online competitors. But it’s a nationwide trend.

In the current recession, I expect retail to be a leading sector, not a lagging one. But I do not think that retail will come back to pre-recession levels in terms of employment. I think a lot of small retailers are going to be driven out of business and are simply not going to come back.

In the Great Recession, those retailers that were driven out of business, did come back. I’m not sure that’s going to happen this time.

J. Douglas Wellington

J. Douglas Wellington is an associate professor of finance at Bangor’s Husson University and a resident of Castine. Wellington oversees the Husson Stock Index, a roster of 29 publicly traded companies that are headquartered in Maine or have a significant number of employees in Maine and can be used to help analyze the state’s economic well-being. This transcript has been edited for length and clarity.

Meg Robbins: Tell me about the trends you’ve been observing in the Husson Stock Index recently. From your perspective, what are the vulnerabilities of Maine’s economy and do you think the federal CARES Act initiatives can sufficiently get the state’s economy back on track?

J. Douglas Wellington: I think the vulnerabilities of Maine’s economy are sort of shown by the Husson Stock Index. I looked at the companies and compared the February 21 stock prices to the March 20 stock prices, which is when we had the huge decrease and things just went south very quickly. Then I looked at which ones sort of recovered up through May 1.

Not surprisingly, the index as a whole during that period went down about 34 percent. But there were significant decreases. The largest one was Penn National Gaming, which went down 79 percent. Well, you could understand that — casinos are places that you no longer could enter. The second largest was Darden Restaurants. Again, that’s not surprising that that would be a significant decrease. That went down 68 percent. Then you have Unum, which went down about 65 percent. Now you’re talking about basically healthcare, insurance and things like that — that’s not surprising because of the possible insurance claims coming out of everything that’s happening. And then finally, WEX Inc., which is involved with corporate credit cards, that went down about 63 percent.

So, you can certainly see where this COVID recession hit companies that have some presence in Maine, some connection with Maine. And, not surprisingly, the businesses hit are in the areas that you would anticipate — hospitality, the insurance industry.

I think that the CARES Act is probably going to help somewhat. You have the Paycheck Protection Program — there is some benefit if you can open up and hire employees. You’ve got the Federal Pandemic Unemployment Compensation program, which, on one hand is good — it helps people who are unemployed because of COVID-19. On the other hand, as some people have noted, by giving people $600 a week you have an incentive for people not wanting to go back to work.

Unfortunately, that sometimes happens when you have such an emergency and the government has to make a response. There’s always some unintended consequences of legislation in the best of times, and when you’re working in a pandemic situation, things happen. But I think that the CARES Act is going to help overall.

I think the main thing that’s going to help is really opening up the economies again. If we get to the place where we have enough testing or we begin to have vaccines, I think that’s when we’ll really come back.

Robbins: What economic signals would concern you? What are you keeping tabs on right now?

Wellington: Well, obviously the number of new jobless claims — that’s very concerning. What I’ve been looking for is a decrease in jobless claims. Last week, the Associated Press reported that applications for jobless aid declined in 44 states. Unfortunately, it rose in six states, and that went anywhere from Connecticut at 9.5 percent to Maryland at 72.1 percent. Maine was at 111.1 percent, so we had the dubious distinction of having the largest increase in weekly jobless claims, when 44 states were already reporting decreases in jobless claims. I’d certainly like to see that number go down.

I’d also like to see the Consumer Confidence Index start coming up. That’s something I am watching. Sometimes it’s a lagging indicator, but I think in this case it might be a leading indicator. If people begin to think, ‘Hey, we’re turning the corner,’ you may begin to see people going to businesses and spending money. I think as more and more people begin to think that way and begin to have some confidence that we may be getting back to normal, like a lot of economic situations, you end up with a self-fulfilling prophecy. When people feel good, they tend to spend some money, and when they spend money, businesses pick up.

I would also be looking at the Purchasing Managers Index, the PMI. That went down a little bit in March; it plummeted in April. It was the lowest number since 2009, so basically since the last big recession. I’d like to see that coming up. If purchasing managers are beginning to feel better from a company standpoint, that may be an indication that companies are coming back around.

All these indicators will begin to signal — and frankly, you’ll also see it on the street. My wife went to Bangor at the beginning of this week and she said parking lots were full and stores were as full as they could be with social distancing, so I think people may be beginning to get out. Some of those not-really-economic indicators are also going to give a feel for whether or not we’re coming back.

Robbins: Can you expand on what those metrics mean and what their impact will be?

Wellington: Yeah. As the jobless claims go down, as the unemployment rate goes down, obviously, that’s indicating we’re coming back. I’m not an expert in the Purchasing Managers Index, I will say, but basically it’s a survey of 600 industrial companies. It gauges companies’ feelings about how their businesses are going to be doing and what they’re going to do in terms of output, new orders, employment, suppliers, delivery time and stock of items purchased. A reading above 50 indicates an expansion of the manufacturing sector. Below 50 represents a contraction and 50 represents no change. We were right at about 50 for the past year or so. We went down to 36 in April, so we’re talking about a big contraction from the previous month.

Robbins: Given what you’ve just outlined, how long do you think Maine can afford to stay closed?

Wellington: You know, if I knew that [laughs]. I’d love to give you an idea, but I have no idea. Each week that goes by puts more and more stress on Maine’s economy. A big part of Maine’s economy, with an older population, is healthcare. Hospitality and retail are also big parts of the economy, and the longer you go without being able to open up restaurants, the longer you’re able to go without opening up hotels, you’re going to begin to see restaurants closing and maybe small motels or hotels closing.

Small business owners a lot of times don’t have a lot of cash on hand, and to shut down at the beginning of the summer is difficult. The governor’s guidelines for opening up will allow restaurants to open up in June, but if the guidelines say you have to open up at 50 percent — these businesses have fixed costs. Can they operate at 50 percent or are they going to close?

It’s the same thing with lodging. It’s opening up in June, but it’s to Maine residents and out-of-state residents who have completed the quarantine guidelines. Well, if you’re out-of-state, you want to come to Maine and lodge someplace, you don’t want to come to Maine, quarantine for 14 days and then lodge someplace.

I’m concerned that the longer we go, the more businesses are going to be in some significant financial trouble and especially because we have a lot tied into people coming here for the summer. We’re not having cruise ships, we’re closing hotels, closing restaurants. So yeah, I don’t have any crystal ball on that. I’m sorry.

Robbins: Thinking back to the last recession, what businesses, industries or sectors were key to Maine’s recovery? How do you think they will play a role this time around?

Wellington: That’s probably where you’d be better off asking economists. I don’t know, and I wasn’t doing Husson’s stock index at that time.

I think one of the things about past recessions, even in 2000 and 2008 is that there were specific identifiable causes. In 2000, it was a tech bust, because the internet was new and tech companies’ valuations were bid up to crazy amounts. You had a bubble and it burst. In 2008, you had real estate and financial institutions, but even though they might have affected the economy in general, they had a specific economic cause and it didn’t affect the entire economy. You had direct effects and you had indirect effects.

This time, in the United States, anything that wasn’t essential was shut down. Restaurants, lodging, retail — everything was shut down. So you didn’t have a specific industry that was directly affected and others indirectly affected. You had everything directly affected except for certain essential businesses. It’s a lot harder to figure out in that situation how you come back.

I would think that some things will be a little bit easier to come back. From my own perspective, would I go into Dick’s Sporting Goods? Yes. I mean, I’m not normally less than six feet away from anybody at Dick’s Sporting Goods when it is open, so it’d be easy to have social distancing and I would feel pretty comfortable there. It would take me a little bit longer to be comfortable sitting in a restaurant. It would take me longer to go to a concert or a sporting event where I’m sitting right next to people having people right in front of me, people right behind me — and tens of thousands of people.

So, even when the government begins to open up different venues, it’s also going to depend on the psychology of the consumers. There are some things that may not come back right away because people are just naturally cautious. I think retail should be able to come out of this OK once we start up, but restaurants I would guess might take a little bit longer. Things like sporting events and concerts — unless people really want to go to sporting events and have pent-up demand, something like that might take a little bit longer.

Robbins: Is there anything else that you want to add that you think is important to keep in mind? Or anything you’ve found particularly insightful or interesting?

Wellington: One of these days, this too shall pass. We’ve gone through world wars, we’ve gone through a civil war, we went through the Spanish Flu in 1918. We’ve gone through lots of different things and we’ve come out of them, so I know we’re going to come out of this. It’s just wondering when and what changes may occur in the country.

I’ll try a little crystal ball — you have people who, for example, didn’t bank online, didn’t buy online. And retail stores were already having issues — that may be exacerbated because of this. There may be things that actually change people’s behaviors. We don’t know exactly what will happen, but maybe there will be more takeout at restaurants, things like that. Maybe there will be more streaming of content, whether it’s concerts or sporting events. We’ll come out of it, but there may be some changes to the landscape when we’re done. But my crystal ball is very cloudy, so don’t put any money on it.